Welcome, readers! Are you looking to refinance your student loans in 2021? Look no further! In this article, we will explore some of the top options available for refinancing your student loans this year. Whether you’re looking to lower your interest rate, consolidate multiple loans, or simply find a more manageable repayment plan, we’ve got you covered. Let’s dive in and discover the best refinance student loan options for 2021!

Finding the Lowest Interest Rates

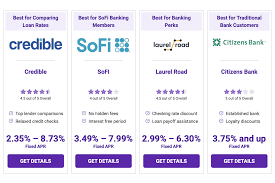

When it comes to refinancing student loans, one of the most important factors to consider is the interest rate. Finding the lowest interest rate can save you a significant amount of money over the life of your loan. So how do you go about finding the best rates?

One of the first steps to finding the lowest interest rates for refinancing student loans is to shop around. Don’t just settle for the first offer you receive. Instead, compare rates from multiple lenders to ensure you are getting the best deal possible. You can use online comparison tools to easily compare rates from different lenders and find the one that offers the lowest interest rate.

Another way to potentially qualify for lower interest rates is to improve your credit score. Lenders typically offer lower rates to borrowers with higher credit scores, as they are considered less risky. If your credit score has improved since you first took out your student loans, you may be able to qualify for a lower interest rate when refinancing.

Additionally, consider choosing a variable interest rate over a fixed interest rate when refinancing your student loans. While fixed interest rates offer stability, variable rates may start out lower and could potentially save you money in the long run if interest rates remain low. However, it’s important to carefully weigh the pros and cons of variable rates before making a decision.

It’s also important to consider the term length of your loan when refinancing. While longer loan terms may result in lower monthly payments, they could also mean paying more in interest over the life of the loan. On the other hand, shorter loan terms may come with higher monthly payments, but could save you money on interest in the long run. Evaluate your financial situation and choose a term length that works best for you.

Lastly, don’t forget to consider any fees associated with refinancing your student loans. Some lenders may charge origination fees or other closing costs, which could offset any savings you would gain from a lower interest rate. Make sure to factor in all costs when comparing loan offers to ensure you are truly getting the best deal.

By following these tips and doing your research, you can increase your chances of finding the lowest interest rates when refinancing your student loans. Saving money on interest can help you pay off your loans faster and achieve financial freedom sooner.

Understanding Loan Terms and Repayment Options

When it comes to refinancing your student loans, it’s essential to have a good understanding of the loan terms and repayment options available to you. This can help you make informed decisions that will benefit your financial situation in the long run.

Loan terms refer to the specific details of your loan agreement, including the interest rate, repayment schedule, and any fees associated with the loan. Understanding these terms can help you determine how much you’ll be paying over the life of the loan and how long it will take to repay the loan in full.

When refinancing your student loans, you have the option to choose a fixed or variable interest rate. A fixed interest rate offers the same rate throughout the life of the loan, providing predictability in your monthly payments. On the other hand, a variable interest rate can fluctuate based on market conditions, potentially resulting in lower initial payments but higher overall costs in the long run.

Repayment options also play a crucial role in managing your student loan debt. Many lenders offer flexible repayment plans that allow you to choose a schedule that fits your budget. Some common repayment options include standard repayment, extended repayment, graduated repayment, and income-driven repayment plans.

Standard repayment plans require you to make fixed monthly payments over a set period, typically 10 years. Extended repayment plans offer a longer repayment term, resulting in lower monthly payments but higher overall interest costs. Graduated repayment plans start with lower payments that increase over time, making it ideal for borrowers expecting their income to rise in the future.

Income-driven repayment plans base your monthly payments on your income and family size, making them a viable option for borrowers experiencing financial hardship. These plans can help lower your monthly payments and offer loan forgiveness after a certain period of time.

It’s essential to carefully review and compare the loan terms and repayment options offered by different lenders before deciding to refinance your student loans. Make sure to consider factors such as interest rates, fees, repayment terms, and borrower benefits to choose the best option that aligns with your financial goals.

Benefits of Consolidating Student Loans

When it comes to managing your student loans, consolidation can be a game-changer. Here are some of the benefits of consolidating your student loans:

1. Simplified Repayment

One of the main advantages of consolidating your student loans is that it simplifies the repayment process. Instead of juggling multiple loans with different due dates and interest rates, consolidation allows you to combine all your loans into one single payment. This not only makes it easier to keep track of your payments, but it can also help you avoid missing any due dates or incurring late fees.

2. Lower Interest Rate

Consolidating your student loans can also potentially save you money in the long run by lowering your interest rate. By consolidating, you may be able to secure a lower interest rate than what you were originally paying on your individual loans. This can result in significant savings over the life of your loan, allowing you to pay off your debt faster and more affordably.

3. Flexible Repayment Options

When you consolidate your student loans, you may also gain access to more flexible repayment options. For example, you may be able to choose a longer repayment term, which can help lower your monthly payments and make them more manageable. Additionally, some consolidation lenders offer income-driven repayment plans, which adjust your monthly payments based on your income level. This can be particularly helpful if you’re struggling to make your current payments and need a more affordable option.

4. Improved Credit Score

Consolidating your student loans can also have a positive impact on your credit score. By consolidating multiple loans into one, you can reduce the number of accounts on your credit report, which can have a positive effect on your credit score. Additionally, if you make consistent, on-time payments on your consolidated loan, you can further improve your credit score over time. This can make it easier for you to qualify for other types of credit in the future, such as a mortgage or car loan.

5. Peace of Mind

Finally, consolidating your student loans can provide you with peace of mind. Knowing that you have a clear plan for repaying your debt and that you have options for managing your payments can help alleviate some of the stress and anxiety that often comes with student loan debt. With a consolidated loan, you can focus on moving forward with your financial goals and making progress towards a debt-free future.

Tips for Choosing the Right Refinance Lender

When it comes to refinancing your student loans, choosing the right lender is crucial. Here are some tips to help you find the best refinance lender for your needs:

1. Research Multiple Lenders: Don’t settle for the first lender that comes your way. Take the time to research multiple lenders to compare their rates, terms, and benefits. Look for lenders that offer competitive rates, flexible repayment options, and good customer service.

2. Check Eligibility Requirements: Before applying for a refinance loan, make sure you meet the eligibility requirements of the lenders you are considering. Some lenders may have minimum credit score requirements or require a certain level of income to qualify for a refinance loan. It’s important to know if you meet these requirements before submitting an application.

3. Consider Loan Terms: When comparing lenders, pay close attention to the loan terms they offer. Some lenders may offer longer repayment terms, which can lower your monthly payments but may result in paying more interest over the life of the loan. On the other hand, shorter loan terms may have higher monthly payments but can save you money on interest in the long run. Consider your financial goals and choose a lender with loan terms that align with your needs.

4. Evaluate Customer Reviews: One of the best ways to gauge the quality of a lender is by reading customer reviews. Look for reviews from borrowers who have refinanced their student loans with the lender you are considering. Pay attention to feedback about the application process, customer service, and overall experience with the lender. Positive reviews can give you confidence in your decision, while negative reviews can help you avoid potential red flags.

5. Compare Interest Rates: Interest rates play a significant role in the cost of your refinance loan. Be sure to compare the interest rates offered by different lenders and choose the one that offers the most competitive rate. A lower interest rate can save you money over the life of the loan, so it’s worth shopping around for the best rate.

6. Consider Additional Benefits: Some lenders offer additional benefits to borrowers who refinance their student loans, such as autopay discounts, career coaching services, or hardship assistance programs. These benefits can add value to your refinance loan and make your experience with the lender more positive. Consider the additional benefits offered by each lender and choose the one that aligns with your needs and preferences.

By following these tips, you can find the right refinance lender for your student loans and save money on your monthly payments and interest costs. Don’t rush the decision – take the time to research, compare, and choose a lender that best fits your financial goals and needs.

How to Start the Refinancing Process

So you’ve decided to refinance your student loans, but where do you start? The first step is to do your research and compare different lenders to find the best deal for your situation. Look at factors such as interest rates, repayment terms, and customer reviews to narrow down your options.

Once you have a shortlist of potential lenders, you’ll need to gather all the necessary documentation to apply for refinancing. This typically includes proof of income, a copy of your student loan statement, and any other relevant financial information. Having all your documents ready will streamline the application process and make it easier for lenders to evaluate your eligibility.

Next, you’ll need to actually apply for refinancing with the lender of your choice. This can typically be done online or over the phone, and the application process is usually straightforward. You’ll need to provide your personal information, financial details, and consent for the lender to perform a credit check.

After you’ve submitted your application, the lender will review your information and determine if you qualify for refinancing. This process can take anywhere from a few days to a few weeks, depending on the lender’s policies and workload. Be sure to check in periodically on the status of your application and provide any additional information requested by the lender.

Once your application has been approved, the lender will work with you to finalize the details of your new loan. This may involve signing new loan documents, setting up a repayment schedule, and transferring the funds to pay off your existing loans. Make sure to review all the terms and conditions of the new loan before signing off to ensure you fully understand the agreement.