Welcome, dear reader! Are you tired of high interest rates and unmanageable terms on your private loans? Refinancing might just be the solution you’ve been looking for. By refinancing your private loans, you can potentially secure better rates and terms that will help you save money in the long run. So, how exactly can you go about refinancing your private loans? Let’s dive in and explore the steps you can take to get better rates and terms on your private loans.

What is Private Loan Refinancing?

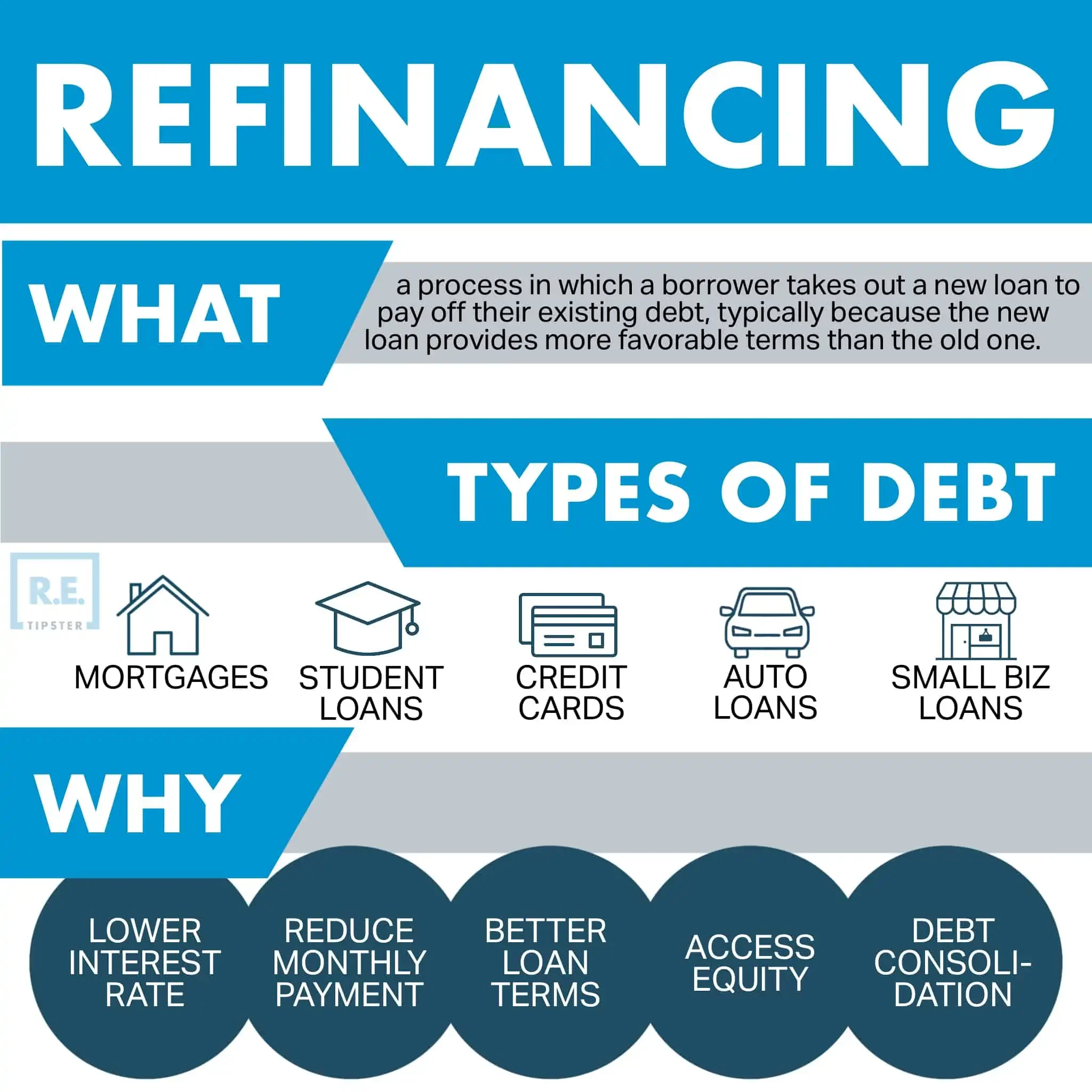

Private loan refinancing is a process that allows borrowers to replace their existing private loan with a new loan that has better terms and conditions. When you refinance a private loan, you take out a new loan to pay off the original loan, often with a lower interest rate or monthly payment. This can help save money on interest payments over the life of the loan and potentially shorten the repayment term. Private loan refinancing is a popular option for borrowers looking to manage their debt more effectively and reduce their financial burden.

When you refinance a private loan, you have the opportunity to shop around for better rates and terms than what you currently have. This can be especially beneficial if your financial situation has improved since you originally took out the loan, as you may qualify for lower interest rates or better repayment terms. Additionally, many private loan refinancing companies offer flexible repayment options, such as a longer repayment term or the ability to make interest-only payments for a certain period.

Private loan refinancing can also help borrowers consolidate multiple loans into one, simplifying their monthly payments and potentially lowering their overall cost of borrowing. By combining multiple loans into a single loan with a lower interest rate, borrowers can save money on interest payments and reduce the stress of managing multiple debts. This can also result in a lower monthly payment, making it easier to budget for other expenses and save for the future.

Overall, private loan refinancing can be a valuable tool for borrowers looking to improve their financial situation and save money on interest payments. By taking advantage of lower interest rates, better terms, and flexible repayment options, borrowers can better manage their debt and work towards achieving their financial goals. If you have a private loan and are struggling to keep up with payments or looking to save money on interest, consider exploring the option of refinancing to see if it could benefit you.

Advantages of Refinancing Private Loans

Refinancing private loans can provide numerous benefits for borrowers looking to improve their financial situation. Among the advantages of refinancing private loans are lower interest rates, extended repayment terms, and improved credit scores.

One of the main advantages of refinancing private loans is the potential to secure a lower interest rate. By refinancing, borrowers may be able to replace their current high-interest rate loan with a new loan that offers a lower rate. This can result in significant savings over the life of the loan, as borrowers will pay less in interest. Lower interest rates can also lead to lower monthly payments, making it easier for borrowers to manage their finances.

In addition to lower interest rates, refinancing private loans can also provide borrowers with extended repayment terms. This means that borrowers may be able to spread out their payments over a longer period of time, resulting in lower monthly payments. Extended repayment terms can help borrowers better manage their cash flow, as they will have more time to pay off their loans.

Another advantage of refinancing private loans is the potential to improve credit scores. When borrowers refinance their loans, they have the opportunity to make on-time payments and improve their credit history. By consistently making payments on their new loan, borrowers can demonstrate to lenders that they are responsible borrowers. This can result in a higher credit score, which can make it easier for borrowers to qualify for future loans at lower interest rates.

Refinancing private loans can also provide borrowers with the opportunity to consolidate their debts. By combining multiple loans into one, borrowers can simplify their finances and make it easier to keep track of their payments. This can reduce the risk of missing payments and incurring late fees, helping borrowers stay on top of their financial obligations.

Overall, there are many advantages to refinancing private loans. From lower interest rates and extended repayment terms to improved credit scores and debt consolidation, refinancing can help borrowers achieve their financial goals and improve their overall financial health.

How to Qualify for Private Loan Refinancing

Private loan refinancing can be a great way to lower your monthly payments or interest rates, but not everyone will qualify for this option. Here are some key factors to consider when trying to qualify for private loan refinancing:

1. Good Credit Score: One of the most important factors that lenders consider when refinancing private loans is your credit score. Lenders typically look for borrowers with good to excellent credit scores, as this shows that you are a responsible borrower who is likely to make on-time payments. If your credit score is less than ideal, you may want to work on improving it before applying for refinancing.

2. Stable Income: Lenders also want to see that you have a stable income that will allow you to make your monthly payments. This means having a steady job or a source of income that is reliable and sufficient to cover your loan payments. If you have recently changed jobs or have irregular income, you may find it harder to qualify for refinancing.

3. Low Debt-to-Income Ratio: Another important factor that lenders consider is your debt-to-income ratio. This ratio compares the amount of debt you have to your income and helps lenders determine if you can afford to take on more debt through refinancing. Ideally, your total monthly debt payments should not exceed 43% of your gross monthly income. If your debt-to-income ratio is too high, you may have trouble qualifying for refinancing.

4. Collateral: Some private lenders may require collateral, such as a home or a car, to secure the refinanced loan. Collateral helps protect the lender in case you default on your loan, and may make it easier for you to qualify for refinancing. However, not all lenders require collateral, so this may vary depending on the lender and your individual situation.

5. Co-signer: If you have trouble qualifying for private loan refinancing on your own, you may want to consider asking a co-signer to help you. A co-signer is someone who agrees to take on the responsibility of repaying the loan if you cannot. Having a co-signer with a good credit score and stable income can increase your chances of qualifying for refinancing and may help you secure better terms and interest rates.

Overall, qualifying for private loan refinancing requires a combination of factors, including a good credit score, stable income, and a low debt-to-income ratio. By taking steps to improve these areas, you can increase your chances of qualifying for refinancing and potentially save money on your monthly payments.

Drawbacks of Refinancing Private Loans

While there are certainly benefits to refinancing private loans, there are also some drawbacks that borrowers should be aware of before making a decision. Here are some important considerations:

1. Loss of Federal Loan Benefits: If you refinance a federal loan into a private loan, you will lose access to federal benefits such as income-driven repayment plans, loan forgiveness programs, and deferment options. These benefits can provide valuable support in times of financial hardship, so it’s important to weigh the potential benefits of a lower interest rate against the loss of federal protections.

2. Potential Fees: Refinancing private loans can involve fees such as origination fees, application fees, and prepayment penalties. These fees can add to the overall cost of the loan and may negate any potential savings from a lower interest rate. Before refinancing, it’s important to carefully review the terms and conditions of the new loan to understand all potential fees involved.

3. Longer Repayment Terms: Refinancing can sometimes extend the term of your loan, resulting in lower monthly payments but ultimately costing more in the long run due to accruing interest over a longer period of time. Borrowers should consider whether they are willing to pay more in interest over the life of the loan in exchange for lower monthly payments.

4. Impact on Credit Score: When you apply for a refinanced loan, the lender will likely perform a hard credit inquiry, which can temporarily lower your credit score. Additionally, closing an old loan and opening a new one can also impact your credit score, as it may alter the average age of your credit accounts and overall credit utilization. A lower credit score can make it more difficult to qualify for future loans or lines of credit, so borrowers should carefully consider the potential impact on their credit before refinancing.

5. Potential Loss of Co-signer Release Options: If you refinance a private loan that you originally co-signed with someone else, you may lose the option to release the co-signer from the loan in the future. This can be particularly concerning for co-signers who were counting on being released from their obligation once the primary borrower’s creditworthiness improved. Before refinancing, it’s important to consider how it may impact any co-signers on the original loan.

In conclusion, while refinancing private loans can offer benefits such as lower interest rates and monthly payments, borrowers should carefully weigh the potential drawbacks before making a decision. It’s important to consider factors such as loss of federal loan benefits, potential fees, longer repayment terms, impact on credit score, and potential loss of co-signer release options before deciding to refinance. By taking the time to thoroughly evaluate all aspects of the refinancing process, borrowers can make an informed decision that aligns with their financial goals and circumstances.

Tips for Choosing the Right Lender for Private Loan Refinancing

When it comes to refinancing private loans, choosing the right lender is crucial. With so many options available, it can be overwhelming to decide which lender to trust with your financial future. Here are some tips to help you choose the right lender for private loan refinancing:

1. Do Your Research: Before committing to a lender, take the time to research and compare different options. Look at interest rates, fees, and customer reviews to get a sense of each lender’s reputation.

2. Check for Prepayment Penalties: Some lenders charge prepayment penalties if you pay off your loan early. Make sure to ask about this before signing any agreements, as it could end up costing you more in the long run.

3. Consider Customer Service: Good customer service is essential when dealing with financial matters. Choose a lender that is responsive, helpful, and willing to answer any questions you may have throughout the refinancing process.

4. Look for Flexibility: It’s important to choose a lender that offers flexible repayment options. Look for lenders that allow you to choose your repayment terms and provide options for deferment or forbearance in case of financial hardship.

5. Evaluate the Loan Terms: When choosing a lender for private loan refinancing, it’s essential to carefully evaluate the loan terms offered. Consider the interest rate, loan term, and any fees associated with the loan. Make sure to calculate the total cost of the loan over time to determine which option is the most affordable.

By following these tips, you can make an informed decision when choosing a lender for private loan refinancing. Remember to research, compare options, and consider factors such as customer service and loan terms to find the best lender for your financial needs.